Changing Economic Landscapes and Worldviews

I was reading an interesting paper called "Depression Babies: Do Macroeconomic Experiences Affect Risk-Taking." The economists examined whether macro-economic circumstances over an individual's lifetime affects their own economic behavior.

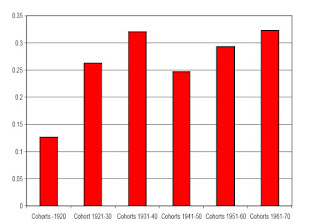

They do an detailed empirical analysis using individual data spanning 40 years, but here's a simple graph that provides interesting evidence.

We see that the stock market participation rates (whether a person has invested in directly held stocks or funds) for the generation that experienced the 1930s Great Depression as young adults ("cohorts 1920s" i.e. born in the 1920s) is significantly less than those born later. The authors do control for confounding factors and things like effects of age or time trends.

I wonder what the implication of India's rapid macro-economic change will be on generations of youth? A 13 year old today, born in 1995 has really experienced a different India. For example, the proliferation of consumer choice-- would teenagers believe that there were basically 4 types of cars, 1 domestic airline, 1 radio station and 2 TV stations 20 years ago?

I wonder what the implication of India's rapid macro-economic change will be on generations of youth? A 13 year old today, born in 1995 has really experienced a different India. For example, the proliferation of consumer choice-- would teenagers believe that there were basically 4 types of cars, 1 domestic airline, 1 radio station and 2 TV stations 20 years ago?

Exposure to global media and good and a dramatically expanded private sector has changed the landscape of opportunities, ideas and has to have shaped a child's worldview. I think today's Indian teenager has different economic expectations and attitudes towards risk than even just a generation before. Growing up in a booming, globally assimilated economy stirs one's imagination, expands visions, creates ideas encourages entrepreneurship, risk-taking and innovation, all feeding back into more growth and prosperity.

"In particular, we test whether individuals who experienced low stock-market returns are less willing to invest in stocks and express more risk aversion, and whether individuals who lived through high-inflation periods are wary of investing in long-term bonds."

They do an detailed empirical analysis using individual data spanning 40 years, but here's a simple graph that provides interesting evidence.

We see that the stock market participation rates (whether a person has invested in directly held stocks or funds) for the generation that experienced the 1930s Great Depression as young adults ("cohorts 1920s" i.e. born in the 1920s) is significantly less than those born later. The authors do control for confounding factors and things like effects of age or time trends.

I wonder what the implication of India's rapid macro-economic change will be on generations of youth? A 13 year old today, born in 1995 has really experienced a different India. For example, the proliferation of consumer choice-- would teenagers believe that there were basically 4 types of cars, 1 domestic airline, 1 radio station and 2 TV stations 20 years ago?Exposure to global media and good and a dramatically expanded private sector has changed the landscape of opportunities, ideas and has to have shaped a child's worldview. I think today's Indian teenager has different economic expectations and attitudes towards risk than even just a generation before. Growing up in a booming, globally assimilated economy stirs one's imagination, expands visions, creates ideas encourages entrepreneurship, risk-taking and innovation, all feeding back into more growth and prosperity.

posted by Ishani | 2:01 PM

|

5 comments

![]()

![]()